Retirement can last decades, which means your savings must work just as long. According to the U.S. Census Bureau, the average life expectancy in the United States now exceeds 76 years. That reality makes income planning a serious priority. A single source of income may not provide enough stability over time. Diversifying income streams can reduce stress and support financial confidence.

A strong retirement strategy centers on creating dependable income that lasts long after your working years end. Relying on a single account or benefit can leave gaps over time. Thoughtful Retirement Planning encourages a mix of income sources that work together to provide balance and stability. The sections below outline seven options that can help support steady cash flow and long-term financial security.

1. Social Security Benefits

Social Security provides a foundation for many retirees. Monthly payments offer a predictable income that adjusts for inflation. Timing plays a critical role in maximizing benefits.

Delaying benefits may increase monthly payouts. Reviewing eligibility age and benefit estimates helps guide decisions. While Social Security rarely covers all expenses, it serves as a stable base within a broader long-term financial strategy.

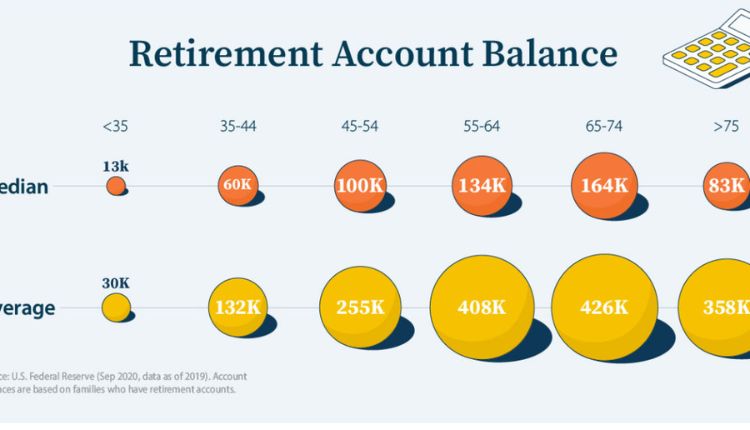

2. Employer-Sponsored Retirement Accounts

Workplace retirement plans, such as 401(k) accounts, usually form a significant portion of savings. These accounts grow through contributions and investment returns over time.

Key considerations include:

- Reviewing asset allocation

- Understanding withdrawal rules

- Monitoring required minimum distributions

- Evaluating tax implications

Careful withdrawal planning ensures funds last throughout retirement. Coordinating distributions with other income sources prevents unnecessary tax strain.

3. Individual Retirement Accounts

Individual Retirement Accounts provide additional flexibility. Traditional and Roth options offer different tax advantages depending on income and timing.

These accounts allow retirees to adjust withdrawal strategies based on market conditions. Strategic use of IRAs supports long-term income planning. Including IRAs in Retirement Planning creates greater control over taxable income levels each year.

4. Investment Portfolio Income

Investments outside retirement accounts can generate dividends, interest, and capital gains. A diversified portfolio reduces reliance on any single asset class.

Portfolio income may include:

- Dividend-paying stocks

- Bonds and fixed-income securities

- Real estate investment trusts

- Mutual funds with an income focus

Regular portfolio review ensures alignment with risk tolerance. Balanced investment income supports steady cash flow without excessive exposure.

5. Rental Property Revenue

Real estate can produce monthly rental income. Properties may appreciate over time while generating cash flow. However, ownership involves management responsibilities and maintenance costs.

Retirees should evaluate property location and market stability. Reliable tenants and consistent occupancy strengthen income reliability. Rental revenue adds diversification when combined with traditional investment accounts.

6. Part-Time or Consulting Work

Some retirees choose to remain professionally active. Part-time work or consulting provides supplemental income and maintains social engagement.

Flexible work arrangements allow retirees to manage hours according to personal preference. Income earned during early retirement years may reduce pressure on savings. Continued activity also helps preserve skills and personal fulfillment.

7. Annuities And Pension Payments

Annuities and pension plans provide a predictable monthly income. Pension benefits from previous employers offer structured payments based on service history.

Annuities convert savings into regular income streams. These products can provide stability, though terms vary widely. Careful evaluation of fees and payout structures is essential before committing funds.

How Expert Guidance Supports Income Stability

- Coordinate multiple income sources to reduce overlap and prevent unnecessary tax burdens.

- Optimize withdrawal timing to extend portfolio longevity and maintain steady cash flow.

- Align investment risk with long-term income needs and personal goals.

- Adjust straegies as life circumstances or tax laws change.

- Create a structured plan that keeps retirement income consistent and sustainable

Retirement income stability depends on thoughtful diversification and disciplined planning. Social Security, employer plans, IRAs, investment portfolios, rental properties, part-time work, and annuities each contribute unique advantages. Retirement Planning connects these sources into a coordinated strategy that balances growth and predictability. By combining multiple income streams, retirees reduce financial uncertainty and strengthen confidence in their long-term financial future.