Most people approaching retirement have spent decades focused on accumulation — building balances, maximizing contributions, and watching portfolios grow. The logic is straightforward during the working years: time is on your side, and market downturns are eventually absorbed by recovery. What changes in retirement is the direction of the cash flow. Instead of adding money to a portfolio, you are drawing from it. That reversal sounds simple, but it introduces a category of risk that standard retirement literature rarely explains with the clarity it deserves.

Sequence-of-returns risk is not a fringe concern. It is one of the most consequential variables in determining whether a retirement portfolio lasts as long as the retiree needs it to. Understanding how this risk works — and how it interacts with structured income planning — is essential for anyone managing or advising on retirement finances in a serious way.

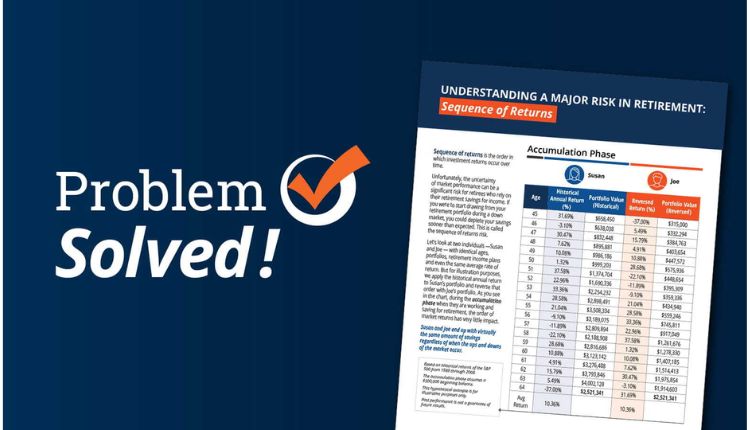

What Sequence-of-Returns Risk Actually Means in Practice

When financial professionals discuss fidelity retirement income planning, the conversation often centers on withdrawal rates, asset allocation, and projected longevity. These are legitimate planning inputs. But they can create a false sense of security if they treat average returns as reliable proxies for how a portfolio will actually perform over a retirement that may last two or three decades.

Sequence-of-returns risk refers to the danger that poor investment returns occurring early in retirement — when withdrawals have already begun — can permanently impair a portfolio’s longevity, even if average returns over the full period appear adequate on paper. The order in which returns arrive matters enormously when you are simultaneously withdrawing principal.

Consider two retirees with identical average annual returns over a twenty-year period. One experiences strong returns in the early years and weaker returns later. The other faces the reverse. Their average returns are the same. Their outcomes are not. The retiree who encounters poor returns early, while also drawing down the portfolio for living expenses, sells more shares at depressed prices to meet withdrawal needs. Those shares are no longer available to participate in any eventual recovery. The other retiree, with strong early returns and a larger asset base before the downturn arrives, is far more insulated from that same decline.

This asymmetry is not captured in most retirement income projections that rely on average return assumptions. It is a structural feature of how portfolios behave under distribution, not a rare edge case.

Why Standard Projections Can Be Misleading

Retirement income projections built on average or median return assumptions present a statistically plausible scenario but not a sequentially realistic one. Markets do not deliver average returns each year. They deliver volatile, uneven returns that may cluster in ways that are either favorable or damaging depending on the timing of your withdrawals.

Monte Carlo simulations — which many planning tools use to model probability distributions of outcomes — are more sophisticated than simple average-return projections, but they still have limitations. They rely on historical return distributions and assumptions about volatility that may not hold in specific market environments. They also do not always account for behavioral responses to portfolio drawdowns, such as reducing or suspending withdrawals, which can alter outcomes significantly.

The practical implication is that a plan showing a high probability of success under modeled conditions may still fail under conditions that are plausible but not well represented in the model. Early in retirement, the margin for error is narrower than most retirees expect.

The Compounding Problem of Early Withdrawals During Downturns

When a portfolio declines in value and withdrawals continue at the same dollar amount, the percentage of the remaining portfolio being withdrawn increases. A fixed withdrawal that represented a reasonable rate against a full portfolio suddenly represents a much larger draw against a depleted one. This acceleration is self-reinforcing: as the portfolio shrinks, each subsequent withdrawal claims a larger share of what remains, leaving progressively less to recover when market conditions improve.

This dynamic means that a bear market in the first few years of retirement carries a fundamentally different consequence than the same bear market occurring ten or fifteen years into retirement. Late-retirement downturns, while unpleasant, occur against a backdrop of reduced time horizon and a portfolio that has already weathered years of distributions. Early-retirement downturns strike when the portfolio is at its largest and the withdrawal period is at its longest.

How Income Planning Structures Can Buffer This Risk

The most direct response to sequence-of-returns risk is not to change where assets are invested — though that matters — but to change the structure of how income is generated during retirement. A portfolio that requires full liquidation of equities to fund annual expenses has no buffer during market downturns. A portfolio structured with deliberate income tiers operates differently.

Income bucketing, sometimes called time-segmentation, is one approach. It involves separating assets into categories based on when they will be needed. Near-term income needs — typically covering the first several years of retirement — are held in lower-volatility, more liquid instruments. Longer-term assets remain invested in growth-oriented holdings. The logic is that near-term expenses do not need to be funded by selling equities during a downturn, because a separate reserve exists for that purpose.

This structure does not eliminate market risk. It creates a buffer of time — enough time, in most cases, for equity markets to recover before the growth portion of the portfolio needs to be tapped for income. The buffer does not guarantee outcomes, but it meaningfully reduces the pressure to sell at the worst possible moment.

The Role of Guaranteed Income in Managing Sequence Risk

Sources of guaranteed income — Social Security, defined benefit pensions, and certain annuity structures — play a specific functional role in managing sequence-of-returns exposure. When a portion of retirement expenses is covered by income that does not depend on portfolio performance, the required withdrawal rate from invested assets is lower. A lower required withdrawal rate means the portfolio has more flexibility to remain invested during downturns rather than being liquidated to cover basic costs.

The decision about when to begin Social Security benefits is, in part, a sequence-of-returns decision. Delaying Social Security increases the guaranteed monthly benefit, which reduces the portfolio withdrawal burden in later years. Whether that trade-off makes sense depends on health, other income sources, and the specific structure of the overall retirement plan — but understanding it as a risk-management tool, not just an income-maximization calculation, changes how the decision is framed.

According to the Social Security Administration, delayed retirement credits can substantially increase monthly benefits for those who wait past their full retirement age, which has direct implications for how much a retirement portfolio is required to produce on its own.

Withdrawal Rate Flexibility as a Risk Reduction Tool

Fixed withdrawal strategies — where a retiree takes the same inflation-adjusted dollar amount each year regardless of portfolio performance — are clean in theory but rigid in practice. They do not allow the portfolio to adapt to poor early returns. Variable withdrawal strategies, by contrast, allow spending to adjust modestly in response to portfolio performance. In years following significant declines, withdrawals are reduced. In stronger years, they may increase.

This flexibility does not require dramatic lifestyle changes. Even modest reductions in discretionary spending during down markets can meaningfully extend portfolio longevity. The behavioral willingness to make those adjustments is, frankly, as important as the technical structure of the plan itself.

What Structured Retirement Income Planning Does and Does Not Solve

Structured income planning addresses the timing and sourcing of withdrawals. It creates buffers against forced liquidation. It integrates guaranteed and variable income sources in a deliberate way. What it does not do is eliminate the underlying market volatility that produces sequence-of-returns risk in the first place.

There is no planning approach that removes all exposure to adverse outcomes in retirement. A sufficiently severe or prolonged bear market early in retirement can stress even well-structured plans. What structured planning does is reduce the severity of that stress, extend the period over which a portfolio can remain functional, and create decision points — rather than forcing a single high-stakes response to bad market conditions.

The retiree who has thought through these dynamics in advance is not insulated from market losses. But they are far better positioned to respond to those losses without compounding them through reactive decisions made under financial pressure.

Closing Perspective

Sequence-of-returns risk is not the most visible topic in retirement planning conversations, but it is one of the most operationally significant. The mechanics of how early retirement returns interact with ongoing withdrawals determine outcomes that no amount of long-term average return data can reliably predict. Understanding this risk is not about being pessimistic about markets — it is about being structurally prepared for the reality that retirement portfolios operate in a fundamentally different mode than accumulation portfolios.

The brochures and generic planning tools that dominate initial retirement conversations tend to simplify this in ways that can leave retirees underprepared. Coordinating guaranteed income sources, structuring withdrawal timing, building near-term income reserves, and maintaining flexibility in spending are all practical, low-drama responses to a real and quantifiable risk. None of them require predicting market behavior. They require acknowledging that the sequence of returns — not just the average — is what a retirement portfolio actually has to live with.

For anyone taking a more detailed look at how income planning frameworks address these dynamics, resources focused on fidelity retirement income planning offer a useful starting point for understanding how different withdrawal structures and income sources interact over a multi-decade retirement horizon. The goal, ultimately, is a retirement that holds up not just in favorable conditions, but in the ones that aren’t.