Unexpected expenses rarely arrive at a convenient time. A car repair, an urgent medical bill, or a temporary income disruption can force stressful decisions if you do not have cash available. An emergency fund is a practical buffer that helps you cover the unexpected without turning to high-interest debt or pulling money from long-term goals. It is not flashy, and it is not meant to maximize returns. Its real value is flexibility: it buys you time to make a calm choice instead of a rushed one.

For beginners, the biggest questions are straightforward: how much should you set aside, and where should you keep it so it is safe and easy to access. The best answers depend on your lifestyle, your monthly obligations, and how stable your income is. With a clear target and a simple system, building an emergency fund becomes less intimidating and more manageable over time.

What An Emergency Fund Is (And What It Is Not)

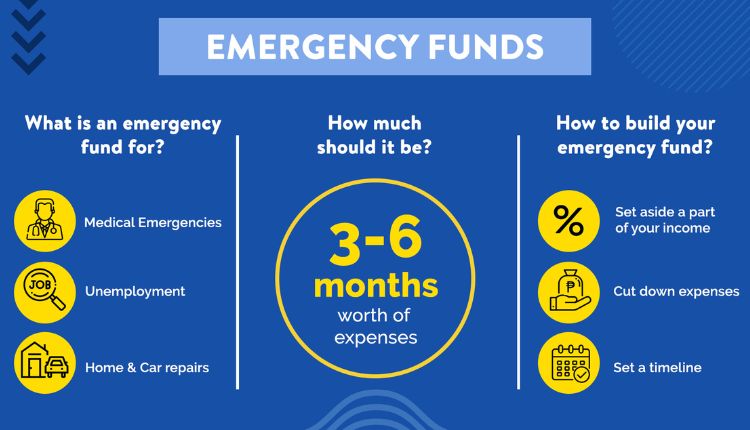

An emergency fund is money reserved for unplanned, necessary expenses that cannot wait. Think job loss, a major repair, travel for a family emergency, or a deductible you need to pay quickly. It is different from savings for predictable costs, such as holiday spending, annual insurance premiums, or a planned home project. Those “known expenses” are still important, but they are not emergencies because you can plan for them.

A helpful rule is to ask: Is this expense unexpected, essential, and time-sensitive? If the answer is yes, your emergency fund may be the right tool. If the expense is expected or optional, it often belongs in a separate savings bucket. Keeping those categories separate protects your emergency money from getting used for everyday wants or planned purchases.

How Much You Need: A Beginner-Friendly Range

A common starting goal is three to six months of essential expenses. “Essential” means the bills you must pay to keep life running: housing, utilities, groceries, transportation, insurance, and minimum debt payments. From there, your situation determines whether you lean closer to three months or closer to six.

You might aim toward the higher end if your income fluctuates, your job feels less secure, or your household relies on one primary earner. You might be comfortable closer to the lower end if your income is stable, your fixed expenses are relatively low, and you have additional backup resources you could use in a pinch.

If three to six months feels overwhelming, build in stages. Start with a starter fund that covers one smaller disruption, like a car repair or a deductible. Then work toward one month of essentials. After that, you can expand to three months and continue until you reach your longer-term target. Progress matters more than perfection, especially early on.

Where To Keep It: Safe, Accessible, And Separate

Emergency funds should be easy to access and stable in value. That means the best home is usually a cash-based account that lets you withdraw money quickly without penalties or market risk. For many people, a high-yield savings account is a strong option because it can earn interest while keeping funds accessible. A money market account can also work well, particularly if you value features like check-writing or a debit card.

Some people prefer a simple two-layer setup. They keep a smaller amount in the account that is easiest to access immediately, then store the rest in a separate high-yield savings account. If a larger expense hits, they transfer money over. This approach can reduce the temptation to spend the full fund while still keeping it available when it matters.

No matter which account you choose, watch for common friction points: monthly fees, minimum balance requirements, and transfer delays. The goal is to make the money easy to reach in a true emergency, while keeping it separate enough that you are not constantly dipping into it.

Places To Avoid for Emergency Savings

Because an emergency fund has a specific job, there are a few places it usually does not belong. The first is the stock market. Investments can go down right when you need the money, which may force you to sell at a loss. Emergency savings should not depend on the market cooperating.

Certificates of deposit can also be tricky. Some CDs charge penalties if you withdraw early, which is exactly what you might need to do in an emergency. Checking accounts are another common mistake. They are convenient, but they tend to earn little interest, and the money can be too easy to spend. Finally, storing large amounts of cash at home is risky due to theft, loss, or damage, and it does not earn anything.

In short, if an option adds volatility, delays access, or introduces penalties, it is usually not the right place for emergency money.

How To Build the Habit and Keep It Working

The most reliable emergency funds are built through routine, not willpower. Automating a transfer, even a small one, is often the simplest way to keep progress steady. You can also look for natural funding sources: a portion of a bonus, a tax refund, or money that becomes available after paying off a loan. The key is consistency. A modest amount saved regularly often beats an ambitious plan that is hard to maintain.

It also helps to define what counts as an emergency before one happens. If your definition is too broad, the fund disappears. If it is too strict, you might avoid using it when you truly should. A balanced definition usually includes essential expenses and income disruptions, but excludes routine overspending or non-urgent wants.

Finally, revisit your target once or twice a year. Expenses change, families change, and income can become more or less predictable. Adjusting your emergency fund is normal and responsible. If you want a second opinion on how your emergency savings fits alongside debt payoff and long-term investing, you might talk it through with financial advisors in Denver or with professionals in your own community, focusing on clarity, tradeoffs, and a plan you can follow.

Conclusion

An emergency fund is one of the most practical financial foundations you can build. It reduces stress, limits debt, and helps protect your long-term goals from short-term surprises. Aim for a realistic target based on essential expenses, keep the money somewhere safe and accessible, and build it through simple, repeatable habits. Over time, that cushion can turn unexpected events into manageable inconveniences, rather than financial turning points.